What Public Company CEOs, CFOs Need to Know About After-Hours Trading

As much as CEOs and CFOs know that they should focus on the long-term performance of their stocks, it’s impossible not to at least notice and wonder about day-to-day, hour-to-hour fluctuations, especially when they seem arbitrary and divorced from fundamentals.

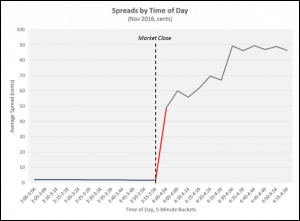

Trading before the market opens and after it closes can be particularly confusing. For instance, outside of the regular market session, spreads can widen dramatically (see chart).

Source: IEX

This kind of wide divergence begs the question: Should public company CEOs and CFOs care about pre-and post-market trading? What is driving these dynamics? And how are exchanges involved?

I had the opportunity to speak with Jay Fraser from IEX, America’s newest stock exchange, to help shed some light on these questions. His answers are provided below. For a deeper conversation, feel free to get in touch.

What is pre- and post-market trading?

The regular market session opens at 9:30 a.m. ET and closes at 4:00 p.m. ET. However, exchanges and some alternative trading systems (ATSs) support trading before and after that regular market session. The hours supported vary by venue and start as early as 4:00 a.m. Anyone can participate in the pre- and post-market sessions on exchanges.

In general, there isn’t a lot of volume outside of the regular market session on a typical day. Once you take out the opening and closing auctions, which together account for about 5%-7% of daily market volume on average, the pre-market and post-market sessions together contribute less than 4% of volume. While there are some anomalous days when after-hours volume is elevated, in general we’re talking about a fairly small portion of overall trading.

That being said, because trading during these periods appeals to different participants and can result in different stock behavior than you are used to, it’s important to understand what is shaping the market during these sessions.

How are the pre- and post-market different than the regular market session?

- Lighter regulation. A number of key regulations designed to protect investors are not applied outside of regular market hours. For example, Regulation NMS’s “Order Protection Rule,” which is designed to prevent trades from occurring at suboptimal prices by prohibiting trading through a better price offered on an exchange, is not enforced during pre- and post-market sessions. Similarly, the Limit Up-Limit Down (LULD) mechanism that prevents trades from occurring outside of specified price bands is only in effect from 9:30 a.m. ET to 3:45 p.m. ET.

- Lower liquidity. In general, there is less volume traded outside of regular market hours. This can make it more difficult to execute trades and can also result in volatility that would be atypical during the regular market session. Additionally, the vast majority (over 90%) of after-market trading does not take place on the exchanges – for the most part they occur “upstairs” (broker internalization when they have both buyer and seller) and retail wholesale platforms (for comparison, during the regular market session, between 36%-38% of volume typically trades off exchange).

- Fewer participants. Some market participants choose not to participate in the pre- and post-market due to higher risk and volatility during those sessions. In fact, according to the SEC, many of the traders participating are professional traders. These participants are more likely to understand and take advantage of the complex dynamics present during these sessions.

The factors above are intertwined. For instance, because there is lighter regulation outside of regular market hours, some long-term investors avoid participating, which, in turn, decreases liquidity, reinforcing the whole cycle. One independent broker quoted in Reuters even called after-hours trading “a bit of a Wild West.” In fact, in its rule book (Rule 3.290), IEX requires that its Members – the broker-dealers who trade directly on IEX – disclose the risks to their customers before accepting any orders to execute during the pre- or post-market.

These factors can create an environment where certain market participants can exploit the wider spreads and lack of liquidity and regulatory safeguards for their own benefit. For example, in this environment, it can be easier for market participants to intentionally move stock prices for their own benefit. Additionally, the rules an exchange sets for its opening and closing auctions will drive behavior in the pre- and post-market sessions, as participants position themselves specifically for the auctions.

How can these dynamics be controlled?

The best way to handle the stress of after-market trading is to remember that, for the most part, your larger, longer-term oriented investors likely aren’t participating in a meaningful way and that the “noise” created by the factors above will likely level out during the next regular market session.

However, some trading venues, including IEX, have put structures in place to try to “tame” the Wild West of pre- and post-market trading and prevent predatory behaviors.

For example:

- Honoring Regulation NMS: While it isn’t required, IEX has chosen to adhere to Reg NMS’ “Order Protection Rule” during the pre- and post-market session, which as we mentioned earlier, is designed to prevent trades from occurring at suboptimal prices. Some other exchanges have also opted to put similar protections in place.

- Consistent Price Protections: In addition to adhering to Reg NMS in the pre- and post-market sessions, IEX has also put certain controls in place that keep non-displayed orders from posting at prices more aggressive than the midpoint. In the pre- and post-market sessions, this is particularly important because spreads are so wide.

- Self-Imposed Order Collars: Finally, IEX has instituted specific “order collars” for the pre- and post-market sessions that prevent an incoming order or an order on the book from actually trading at prices that are more than a certain percentage away from the last sale. While the collars are wider than during the regular market session, they are designed to keep stock prices from getting too volatile.

These features are designed to help mitigate the impact of the dynamics present in the pre- and post-market, and contribute to a more fair and orderly market. Keeping these protections in place during the pre- and post-market sessions has the potential to keep atypical trades from driving volatility in the stock price.

As a CEO, CFO, Treasurer or IRO, what other questions do you have about unusual or surprising trading activity in your stock? Do you understand how the market design decisions made by your listings venue can affect trading outcomes?

IEX launched as America’s newest stock exchange on September 2, 2016 and today regularly matches over 100 million shares daily with a notional value of over $5 billion. IEX plans to begin listing public companies on its exchange in 2017. For more information, contact jay.fraser@iextrading.com.

Mike Piccinino is a Managing Director on Westwicke's medical technology and diagnostics teams. He has extensive experience in the buy-side investment process. He has a BA from James Madison University.

Leave a Reply